Do nice guys finish last? Does it pay to be bad? The stock market has answered with a tepid yes.

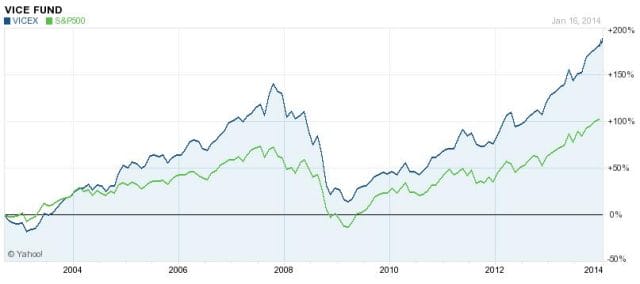

That answer is shown in the above graph, which compares the returns of the Vice Fund over the past decade to the S&P 500, an index often considered representative of the state of the American stock market. The graph shows that the Vice Fund has outperformed the S&P 500 and, one could say, beaten the market.

What is the Vice Fund? As the name indicates, it invests in a collection of sinful stocks. As its managers describe it:

Designed with the goal of delivering better risk-adjusted returns than the S&P 500 Index. It invests primarily in stocks in the tobacco, alcohol, gaming and defense industries. We believe these industries tend to thrive regardless of the economy as a whole.

In a book called Investing In Vice, the fund manager unapologetically lays out a manifesto for investing in industries that would make a priest cringe. As people always gamble, fight, and smoke, he argues that Vice’s investments are “recession proof” and have huge growth opportunities. Think of the growth of defense contractors during a buildup to war, or the new profits to be made in legal weed.

But as pointed out by Slate magazine in 2005, several years into the life of the Vice fund, nice guys don’t necessarily finish last. The virtuous portfolio of the Catholic Values Fund beat the market almost as handedly as Vice. That dynamic remains true today.1

Investing virtuously — or socially responsible investing (SRI) as its known — has an unclear financial track record. A National Post article quotes Professor Geoffrey Heal of Columbia Business School who noted that SRI funds “are not among the top performers, [but] they do perform above average.” But other analysts and studies disagree or find that socially responsible funds have done better or worse at different times, leaving it unclear whether the outcome is a result of random chance or an actual difference in the aggregate performance of socially responsible companies.

(It’s unclear why SRI funds should consistently outperform the market. Instead financial advisors focus on diversifying socially responsible funds enough that they can safely match the performance of the wider stock market.)

That said, the purity of the Vice fund and its virtuous counterparts seems to be lacking. Salon’s look at the portfolio of the Catholic Values Fund revealed that it shared investments in defense contractors with the Vice Fund. At the same time, the Vice Fund’s investments in Berkshire Hathaway and Microsoft don’t seem particularly evil. And as Investing In Vice points out, Anheuser-Busch, maker of Budweiser, is a staple sin stock, yet it is also a top recycler. Dividing the market into saints and sinners seems to be a difficult task.

The Vice Fund does make some evil sounding investments. It profited from betting that the school shooting in Newtown would increase demand for firearms and its manager likes cigarette investments because the product is addictive. But as the fund managers say, vices are not crimes. The fund also likes smartphone and coffee investments because they are addictive. And it does not try to find the next Enron and sell just before the financial fraud is discovered, nor invest in JP Morgan in admiration of its ability to pay its way out of Justice Department lawsuits.

In fact, sinful investing seems much more Warren Buffett than Lex Luthor. In Investing In Vice, the the Vice Fund’s former manager refutes the “go-go days of Wall Street” while citing investment lessons like “don’t invest in what you don’t understand.” He recommends stocks in liquor, tobacco, and porn because they offer the same “slow, steady, boring returns” of Procter & Gamble, the company responsible for making your toothpaste, laundry detergent, and diapers. Stock tips site Insider Monkey recommends ignoring the Vice Fund not for moral reasons, but because it does not outperform the market enough to justify the fund’s 2% management fees.

In fact, the recession refuted the Vice Fund’s claim that a portfolio of “booze, bets, bombs, and butts” is recession proof. While the fund did beat several market indices, the above graphs show that the fund tumbled during the recession in 2008-2009 just like the rest of the market. Perhaps the Vice Fund’s leadership should listen to the sex workers interviewed by The Economist for a report on the “deep recession” in the prostitution business:

And Vivienne, an independent escort in the south who works part-time to supplement her income as a photographer, says paying for sex is a luxury: “Food is more important; the mortgage is more important; petrol is more important.” She is offering discounts out of desperation, reckoning it is better to reduce prices by £20 ($30) than to have no customers at all.

Given that we turn to vices as an escape, it’s understandable to think that they follow different rules. But if the Vice Fund’s experiment in sinful investing has a lesson, it’s that this is not the case.

This post was written by Alex Mayyasi. Follow him on Twitter here or Google Plus. To get occasional notifications when we write blog posts, sign up for our email list.

1Both also beat the Dow. But the Nasdaq performed better than both the Vice and the Catholic Values Fund.