“I’ve learned many things from [George Soros], but perhaps the most significant is that it’s not whether you’re right or wrong, but how much money you make when you’re right and how much you lose when you’re wrong.”

Stanley Druckenmiller, 1994

* * *

In 1992, George Soros brought the Bank of England to its knees. In the process, he pocketed over a billion dollars. Making a billion dollars is by all accounts pretty cool. But demolishing the monetary system of Great Britain in a single day with an elegantly constructed bet against its currency? That’s the stuff of legends.

Though it occurred just two decades ago, Soros made his nation-shaking bet in a very different time. Back then, hedge funds hadn’t yet entered the public consciousness, restrictions on capital flowing from one country to another were just lifted, and the era of the 24-hour news cycle had just begun.

To appreciate how Soros made a fortune betting against the British pound requires some knowledge of how exchange rates between countries work, the macroeconomic tools governments use to stimulate economies, and how hedge funds make money. Our readers are invited to correct us if we stumble in explaining any of these concepts.

And so onwards with the story of how George Soros led a group of traders to break the entire foreign currency system of Great Britain—and profit handsomely at the expense of British taxpayers and others who were on the wrong side of the greatest financial bet of the 20th century.

Picking Up the Pieces in Europe

Let’s start by laying out the historical backdrop for Soros’ gambit. After Word War II, European countries wanted to integrate their economies more tightly with each other. The hope was that tighter relations would prevent catastrophic wars from breaking out every few decades and create a Pan-European market that could compete with the United States. This culminated in the European Union (EU), which didn’t assume its current form with a single currency until 1999.

A precursor to the EU was the European Exchange Rate mechanism (ERM), which was created in 1979. Countries weren’t ready to give up their national currencies, but they agreed to fix their exchange rates with each other instead of “floating” their currency and letting capital markets set the rates. Since Germany had the strongest economy in Europe, each country set their currency’s value in Deutschmarks. They agreed to maintain the exchange rate between their currency and the Deutschmark within an acceptable band of plus or minus 6% of the agreed upon rate.

With fixed exchange rates, countries can’t just “set it and forget it.” People trade currency every day, exchanging their currency to buy imports or sell exports, and the market applies pressure based on what it thinks the actual rate should be based on supply and demand for a currency. To keep the exchange rate fixed, governments need to participate in the market and nudge it in the agreed upon direction.

Governments can manage their currency in two main ways. First, they can take their reserves of foreign currency and buy up their own currency on the open market. That causes the currency to appreciate. Doing the opposite devalues the currency.

Alternatively, governments can influence exchange rates by setting interest rates. Want your currency to appreciate? Raise rates to entice people to buy your currency and lend that money at higher interest rates. Want your currency to depreciate? Cut interest rates so capital needs to go elsewhere in search of juicy profits.

Messing around with interest rates is a big deal, however, because interest rates affect the whole economy. Along with government spending, interest rates are the main lever governments can use to adjust the economy. If the country is experiencing a recession, the government might cut interest rates to spur investment and spending. If inflation is high, the government might raise rates to shrink the supply of money.

So, all this is to say that there are consequences to maintaining a fixed exchange rate. It’s an external forcing function that ties governments’ hands on monetary policy, which may limit or even contradict what they need to do to keep the domestic economy healthy.

Britain Enters the ERM

.jpg)

John Major, leading proponent of ERM while serving under Prime Minister Margaret Thatcher. Major was Prime Minister when the chickens came home to roost, so to speak.

In 1990, Britain was a country that arguably could use an external forcing function to tie its hands on monetary policy. Inflation was high, productivity was low, exports were uncompetitive, and no one really believed the government was capable of fixing the issues.

The Prime Minister at the time, Margaret Thatcher, had long opposed entering the ERM, insisting that the price of the pound be set by the markets. By 1990, however, Thatcher lacked the political power to oppose other members of her Conservative party who wanted to fix their exchange rates with the rest of Europe.

The decision to join the ERM was championed by John Major, who was the Chancellor of the Exchequer in Thatcher’s cabinet. In October 1990, Britain finally enter the ERM at an exchange rate of 2.95 Deutschmark (DM) for each British pound (GBP). The British government was obligated to keep the exchange rate within 2.78 DM to 3.13 DM.

Shortly thereafter, Major replaced Thatcher as the Prime Minister. The fixed exchange rate system was to be the centerpiece of his economic plan. Major thought that the ERM would serve as a sort of “autopilot” that kept the British monetary policy on proper course. The government couldn’t play with the money supply willy-nilly because its hands were tied by the exchange rate agreement.

And to a certain extent, the policy worked. Between 1990 and 1992, inflation decreased, interest rates eased, and unemployment was low by historical standards. In 1992, however, England felt the impact of a massive global recession, and unemployment spiked to 12.7% from just 7.7% two years prior.

And so we come to 1992. Ordinarily, Britain could spur investment and spending by cutting interest rates during an employment crisis. But in this case, doing so would push the pound’s value below the agreed upon amount. So while the people of Great Britain dealt with a recession, the government’s hands were tied; they’d just have to ride it out.

Meanwhile in New York City

In 1992, George Soros was 62 years old and led the Quantum Fund, a hedge fund he founded in 1970 that bet on macroeconomic trends. Soros was already a very rich guy, but he wasn’t iconically rich, or the public figure he is today.

If hedge funds have an air of mystery about them today, this was especially true in 1992—it wasn’t until then that the term even entered the popular vernacular.

Mention of the words “Hedge Fund” by Year According to Google Books

What is a hedge fund exactly? Well, the word “hedge” provides a clue to their original purpose: investing capital to make a specific bet that something will happen. Hedge funds also use financial instruments to “hedge” against other risks in order to more clearly isolate the bet that they want to make.

Here’s an example. Say you’re a hedge fund that thinks AT&T’s cell phone network stinks and you want to bet against it. You could “short” the stock (make money when the stock goes down), but the whole cell phone market is going gangbusters, so AT&T might get new customers even though it stinks. If that happens, AT&T’s stock price could go up, and you’d lose a lot of money. To “hedge” against this risk, you buy some Verizon stock as well, because more precisely, you think that AT&T is crappy relative to Verizon.

Now, if cell phone carrier stocks increase in value, you still make money in the event that Verizon goes up more than AT&T does. Conversely, if cell phone stocks go down, you still make money if AT&T’s stock goes down faster than Verizon’s does. By creating a position like this, you’ve “hedged” a lot of the more general market and industry risks away and made a very specific bet: that AT&T stinks compared to Verizon.

Another thing hedge funds do (if they’re pretty sure about their wager) is borrow funds to put even more money behind the bet. On the AT&T-Verizon trade, they might make a little bit of money on each share. But if they use mostly borrowed money, they can buy a lot of shares without fronting much capital. So if you’re really sure a bet is right, you might borrow a lot of money to enhance your payday.

A final thing to note about hedge funds is how their managers get paid. The managers are typically investing other people’s money (rich people, endowments, etc), and they receive management fees to cover the fund’s expenses; this includes a salary. The standard is about 2% of the funds under management. So if you manage a very large hedge fund in terms of the amount of money being invested, you can earn some decent income regardless of how the fund performs. But not enough to make you a billionaire.

Hedge fund managers become billionaires by placing really successful bets. Managers earn around 20% of the returns that the fund creates (assuming the fund meets some minimum benchmark). So if your fund makes a bet that produces a billion dollar return, you and your partners make at least $200 million of that. Do that for a few years, especially if you place larger and larger bets, and voila! You’re a billionaire.

So in short, hedge funds try to make isolated bets using financial instruments. They borrow money to make the potential rewards even sweeter, and hedge fund managers can make boatloads of money when they bet right. And that’s exactly what Soros and his partners were about to do.

A Mis-priced Currency Means Big Opportunity

Photo by deg.io

By the spring of 1992, just a year and a half after Britain joined the ERM, the fixed exchange rate posed a serious problem. While putting on a cheery public face, internally the Exchequer (England’s Treasury department) realized that the currency was mispriced relative to the Deutschemark. Jonathan Portes, an economist who was at the time a junior staff member there, wrote:

“In May 1992, the immediate problem was obvious. From a domestic point of view, the appropriate level of interest rates, given weak demand, was much lower than that necessary to maintain [the] sterling’s position in the ERM.

Moreover, it was becoming increasingly clear that sterling was overvalued; even in the depths of a recession, we still had a large current account deficit [the country was importing more than it exported].

We argued that the fundamental problem was that we’d joined the ERM at the wrong rate; sterling was overvalued, meaning that we were stuck with a structural current account deficit.”

The sterling was priced too high. The British government knew it, and the market knew it too as the pound was trading at the lower end of the agreed upon band with the Deutschemark.

What kept the pound from plummeting in value was the British government’s guarantee that it would keep the value propped up, and the market believed that it would. As long as everyone believed that England would stay indefinitely committed to buying pounds for around 2.95 Deutschemarks, the status quo was maintained.

The Flashpoint

“Markets can influence the events that they anticipate.”

Throughout the summer of 1992, the British pound held its position. That is, until Germany threw Britain under the bus and all hell broke loose.

For some time that year, German central bank officials made comments on and off the record that undermined the sterling’s strength. The British paper The Independent documents the slights:

“On 25 August, for example, Reimut Jochimsen, a Bundesbank council member, issued a speech saying that there was potential for realignment within the ERM. Sterling weakened. On 10 September, an unnamed Bundesbank official was quoted as saying that a devaluation of sterling was inevitable. The pound fell.”

The event that ultimately led to the undoing of the British pound’s fixed exchange rate was an interview with the President of the German Bundesbank, Helmut Schlesinger. Schlesinger gave the interview to the Wall Street Journal and a German newspaper. He had one condition: If they wanted to directly quote him, they had to let him review the quotes. If they only indirectly paraphrased him, no such permission was necessary.

President of the German Bundesbank, Helmut Schlesinger

That night on September 16th, 1992, the following report paraphrasing Schlesinger’s words went out over the newswires:

“The President of the Bundesbank, Professor Helmut Schlesinger, does not rule out the possibility that, even after the realignment and the cut in German interest rates, one or two currencies could come under pressure before the referendum in France. He conceded in an interview that the problems are of course not solved completely by the measures taken.”

By the morning, the report landed on George Soros’ desk. Soros and the entire financial market took this to believe that the pound sterling was one of those currencies that could “come under pressure” and be devalued.

In just one day, this seemingly innocuous, paraphrased quote would bring devastation to the Bank of England and net George Soros over a billion dollars in profit. The market ceased to believe that England would be able to maintain its current exchange rate—and that belief was all that was keeping the pound from falling.

The Trade of the Century

“There is no point in being confident and having a small position.”

Since August, Soros and his Quantum Fund had been building a $1.5 billion position to bet that the price of Sterling would fall. Since the British government’s full faith and credit was stating that it would not fall, this wasn’t necessarily something that was going to happen. But Stanley Druckenmiller, a senior member of the fund, saw the report from Schlesinger and immediately realized its importance.

Sebastian Mallaby’s book More Money Than God recounts the day’s events. According to Mallaby, Druckenmiller noted that their $1.5 billion bet against the pound was about to pay off and that they should consider adding to the position.

Soros retorted with a different strategy: “Go for the jugular.”

If Schlesinger’s quote could be used as the catalyst for the pound to devalue, why shouldn’t today be the day it happened? Instead of slowly building up a short position against the sterling, the Quantum Fund could short sell sterling on an unprecedented scale today. Doing so would not only help hasten the tumble of the sterling, but also increase the fund’s profit.

It was this decision to “go for the jugular” that netted Soros’s firm over a billion dollars, toppled the Bank of England’s currency regime, and ultimately led to the disgrace of the Prime Minister. It also cost the British taxpayers billions.

The man himself, George Soros. Picture from “Charlie Rose”; modified by Priceonomics.

Let’s walk through Soros’s trade to understand why it was so elegant. As we stated earlier, the trade was for the Quantum Fund to “short” the British pound, meaning they would make money if the currency’s value went down.

Now, what exactly does it mean to “short” a currency, or anything for that matter? Let’s say it’s January 2009 and you think Apple’s iPhone is over the hill and that the company’s stock price (of $90) will decline. How do you benefit from this insight?

Well, you or your broker can go to someone that owns some Apple stock and ask to borrow a single Apple stock from them. You’ll give them back the share later and of course pay them interest for the loan. But for now, you sell that stock for $90 in cash. Two days later, the stock price is $88, so you buy one share with your $90 in cash. That leaves you with $2 in profit! (Well almost two dollars—you have to pay the person who loaned you the stock two days of interest.)

But what if you didn’t sell your Apple stock when it hit $88 and instead decided to hold onto it until the stock plummeted further? Well, you’d be screwed because the stock went up from $90 to around $600; you would lose $510 on a the trade, plus interest!

If you buy a stock, the worst you can do is lose all your money. If you short a stock, your downside is limitless because the stock can always keep going up. You can possibly lose more than all your money, and that’s a very bad thing. So if you take a short position, you want to make sure your downside risk is hedged.

And what if you want to short a currency like the British pound? In this case, you’d go to a British person or company and ask to borrow money from them. They say, “Sure, here’s 100 British pounds. Just give me back the pounds in a few days with some interest, and we’ll have some tea and crumpets.” Now, you take those 100 British pounds, and you convert them into 295 Deutschemarks at the agreed upon exchange rate.

At this point, you would really like the British pound to lose value relative to the Deutschmark. Why? Because if the British pound depreciates 10%, when you convert the 295 DM back to pounds to repay the loan, you’ll have 110 pounds. You can pay back the 100 pounds and a little bit of interest, and you’ll still clear about 10 pounds in profit.

So you make money if the pound devalues. But what if the pound appreciates? You’ll lose your shirt. Therein lies the brilliance of Soros’s bet: if the pound tanked, they would make billions on their short. And if the pound increased in value? Well, that scenario was impossible because everyone knew the sterling was over priced. It already traded at the bottom of its trading band, and the only thing that kept it propped up was government intervention. There was no scenario in which the pound would appreciate.

So, either the pound would stay about the same in value (in which case Soros’s fund wouldn’t make any money, but wouldn’t lose that much money), or the pound would be devalued and the firm would make an obscene amount of money. There was no massive downside—only a massive upside.

As The Handbook of Hedge Funds puts it:

“If speculators were to break the ERM, being short the pound could turn out to be a very profitable position. Even if the devaluation did not occur, the chances of seeing the pound strengthen were small — it was more likely to stay at the bottom of its fluctuation band. The only downside for speculators was transaction costs.”

And so that morning, Soros and his fund increased their short position against the British pound from $1.5 to $10 billion. It was the perfect bet with a mitigated downside and a limitless upside. It was like betting on a coin flip, were if the coin lands on heads (the pound devalues), they make a lot of money. If the coin lands on tails (the exchange rates remained fixed), they only lose a small amount of money on loan interest. That’s the kind of bet Soros would pour money into all the day, even if he had to borrow billions.

Fighting off the Speculators

“Our total position by Black Wednesday had to be worth almost $10 billion. We planned to sell more than that. In fact, when Norman Lamont [the British finance minister] said just before the devaluation that he would borrow nearly $15 billion to defend sterling, we were amused because that was about how much we wanted to sell.”

– George Soros, 1992

As Europe slept, Soros borrowed and sold pounds from anyone that he could. The Quantum Fund’s position exceeded $10 billion shorting the pound. Other hedge funds got wind of the trade (and the report from the Bundesbank) and started following suit, also borrowing and selling pounds.

By the time London markets opened for business and British treasury officials started their day, tens of billions of pounds had been sold. The pound was dangerously close to trading below the levels mandated by the ERM.

The Bank of England was about to have a very shitty day.

British officials first responded by buying one billion pounds at 8:40 AM. The purchase had no effect on the price of the pound. The whole world was selling, and the British government didn’t have the buying power to fight it all off. It’s estimated that the British government spent £27 billion of its reserves buying up pounds to no avail.

By 9AM, finance minister Norman Lamont contacted Prime Minister John Major and told him they couldn’t possibly buy up enough pounds to keep the currency propped up. The only option left for the British government to keep their currency trading at the right level would be to increase interest rates dramatically and attract people to buy pounds. Major refused. Britain was in the midst of a recession, and increasing rates would further shrink the economy. It would be political suicide.

Blood was in the water. Global capital continued to bet against the pound. An hour and a half later, Lamont called the Prime Minister to re-plead his case. The Prime Minister relented. At 11AM, the British government announced they would increase interest rates 200 basis points, from 10% to 12%.

How did the value of the pound react to this enormous increase in interest rates? Nothing happened. The pound continued to plummet. Lamont headed to the Prime Minister’s residence to figure out how to salvage the situation, which led them to announce an interest rate increase of another 300 basis points, from 12% to 15%.

What was the effect of this rate increase on the sterling? Again, nothing. As Mallaby later documents in his book, Soros and the gang of speculators knew victory was near:

“At their desks on the other side of the Atlantic, Druckenmiller and Soros saw the rate hikes as an act of desperation by a dying man. They were a signal that the end was nigh–and that it was time for one last push to sell the life out of the British currency.”

The market expected that Britain would have to devalue its currency and that no amount of interest rate hikes or currency purchasing would change that. At this point, the sentiment that Britain would exit the ERM and devalue its currency was a self-fulfilling prophecy; if the speculators believed it enough to put their money behind it, it would eventually come true.

At 7:30 PM that night, Lamont held a news conference to announce that Britain would be exiting the ERM and floating its currency on the market. Soros and the speculators won.

The Aftermath of Black Wednesday

British financial history now refers to September 17, 1992, as “Black Wednesday;” George Soros, however, probably calls it something like “Awesome Wednesday.” Once Great Britain floated its currency, the pound fell 15% versus the Deutschmark and 25% versus the US Dollar.

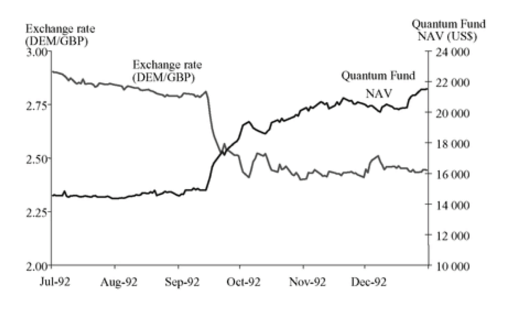

If you’ll remember, Soros’s Quantum Fund had approximately $15 billion betting that the pound would fall versus other currencies. They had borrowed billions to make this trade, and they were right. Here’s what happened to the value of their fund versus the price of the pound:

Source: The Handbook of Hedge Funds

The value of the fund increased almost instantly from $15BN to $19BN when the pound floated; a few months later, the fund was worth almost $22 BN. Remember, this is a hedge fund, so Soros and his partners made at least 20% of that $7 billion upside, which is at least $1.4BN. And that, my friends, is how you become a billionaire.

The nature of Wall Street trading is that if you win big, someone else must lose big. In this case, there was an enormous wealth transfer from the British taxpayers to Soros and other hedge fund managers. The Guardian recounts:

“Jim Trott, former chief dealer for the Bank of England, described the day as “stunningly expensive”. He said that behind the scenes he bought more sterling in four hours that day than anybody had before or since. All of his purchases lost value during the day – and went down even more when the government pulled out.”

In the run up to the devaluation, the British Treasury kept spending its foreign currency on British pounds that become much less valuable after the Treasury floated the exchange rate. To maintain the fiction that the pound was properly priced, it essentially paid a dollar for something everyone knew was going to be worth three quarters. The cost to British taxpayers was estimated at roughly £3.3 billion.

Losing billions of dollars of taxpayer money is so routine for politicians that they may not lose any sleep over the matter. They do, however, care about the political implications of publicly looking like a bunch of incompetents. You can’t make multiple announcements in a single day that you’re massively hiking interest rates in the middle of a recession or completely changing how foreign currency works without giving everyone the impression that you have no idea what you’re doing.

John Major had made entering the ERM the centerpiece of his monetary policy and his plan to bring austerity to England. The events destroyed his credibility. Voters booted Major and his party from power in the next election. As it turns out, Margaret Thatcher was right: the UK had no business trying to artificially prop up its currency in an era when a handful of hedge funds could assemble more capital in a few hours than the Bank of England had at its disposal.

If you’re looking for a take away from this story, that’s one of them. The amount of money sloshing around global markets is so enormous that it can bring even the British government to its knees in one day. Another takeaway is that regulations like this can create unexpected loopholes, and someone more clever than the politicians will eventually spot it.

But perhaps most importantly, this story shows the power of the one-sided bet. In 1992, the bet was a well-designed macroeconomic trade against fixed exchange rates, executed by George Soros and his team. If they were wrong, the downside was almost zero. But they were right, and the upside was unfathomably high.

Bets like that almost never come along, but when they do, enormous transfers of wealth take place from the sheep to the wolves.

Our next article examines the decision of the San Francisco School District to eliminate algebra from middle schools—and the freakout that followed. To get notified when we post it → join our email list.

Priceonomics published an earlier version of this article on May 15, 2014.

![]()

Want to write for Priceonomics? We are hiring a full-time staff writer and looking for freelance contributors.