This post is adapted from the blog of Raltin, a Priceonomics Data Studio customer. Does your company have interesting data? Become a Priceonomics customer.

***

GEICO, the largest brand advertiser in America, spends well over a billion dollars a year to drive home the message that you can save money with GEICO.

While the exact message has evolved over the years, the most common refrain in a GEICO commercial is “15 minutes could save you 15% or more on car insurance.” We’ve all heard it so many times, it’s part of our subconscious at this point.

But is it really true, do you really save 15% or more with GEICO?

We analyzed data from Priceonomics customer Raltin, a finance data company that combed through public insurance filings in eight states to find out if GEICO saves you money. We looked at the quoted rates for drivers with clean driving records and comparable policies to see how GEICO premiums compare to the median in each state.

We found that across the eight states we looked at, GEICO rates were almost 20% cheaper than the state median. In every state we looked at, GEICO was cheaper than the median and the discounts ranged from 12% to 34%.

However, while GEICO is cheaper than the median, it’s not always the cheapest option. We did a deep dive in California and found that both Metromile and USAA were cheaper than GEICO and that it still pays to comparison shop.

***

Before diving into the data, all the analysis below is just on drivers with a “clean” driving record (meaning no recent accidents or tickets), unless otherwise noted. It’s entirely possible among those with more checkered driving histories, the results could be different. Additionally, this data comes from insurance companies filing their rates with state governments in response to survey questions regarding how much they charge drivers based on the policy and drivers characteristics (the car, their history, age).

Source: Raltin

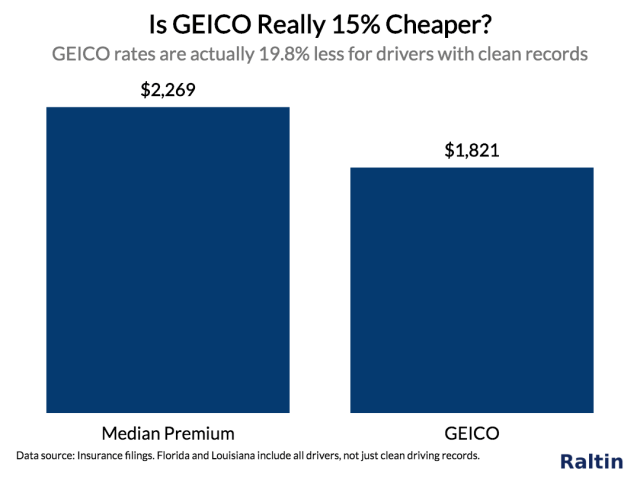

Across the eight states we examined, GEICO was 19.8% cheaper than the median rate in the state.

The median rate across our sample of states was $2,269 per year for a car insurance policy. GEICO, however, was $1,821 per year, a savings of over $400 and 19.8%.

According to this data set, there appears to be some truth to the claim that GEICO can save you over 15% on the your car insurance policy. That rate of savings, however, can vary dramatically by state.

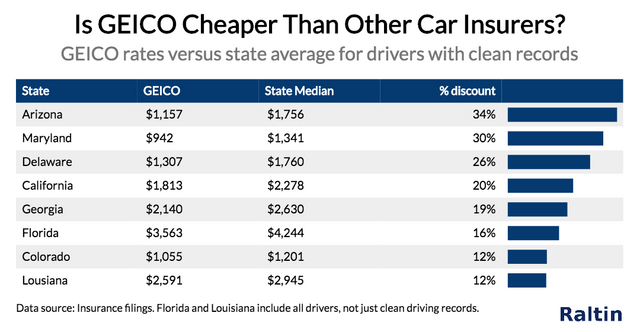

The chart below shows the median GEICO premium versus the state median for drivers with clean driving records, split out by state:

Source: Raltin

In all the states we looked at, GEICO is less expensive than the state median. However, in places like Arizona and Maryland, GEICO savings are over 30% versus the typical insurer in the state. In states like Louisiana and Colorado, the savings are a more modest 12%, but still substantial.

So, if you’re primarily interested in getting the lowest price, should you just go with GEICO since this analysis shows it is less expensive?

Not exactly. This analysis indicates that GEICO is cheaper than the median in the state, but that doesn’t mean it’s always the cheapest option.

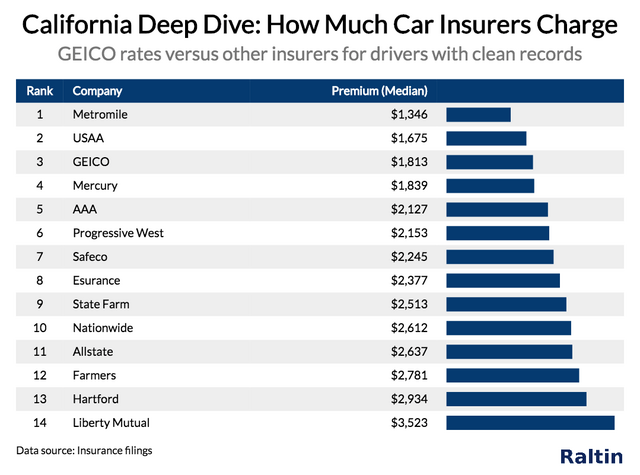

To illustrate this point, let’s do a deep dive in the state of California. The chart below shows the median price of a car insurance policy from popular carriers among drivers with clean records.

Source: Raltin

In California, while GEICO certainly is on the more affordable range of options, it’s not the cheapest according to this data. Metromile, a company that charges based on how much you drive instead of a flat fee, has the lowest median price. USAA, a company that offers policies for military members, veterans, and their families is also slightly cheaper than GEICO in this analysis.

In general, insurance companies’ prices have a wide range so a company with a higher median price, may offer you a discount that GEICO wouldn’t based on your particular circumstance.

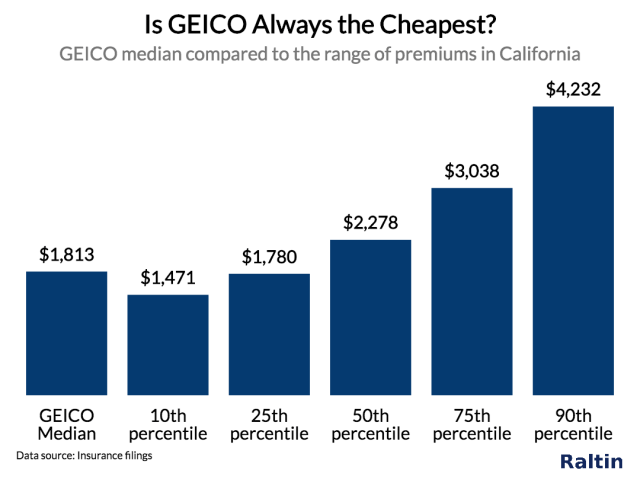

The chart below illustrates the importance of shopping around. The first data point is GEICO, as compared to the price by percentile (10th, 25th, 50th, 75th, 90th) in California.

Source: Raltin

Typically, GEICO is less expensive than the 50th percentile price in California. However, you might get a really good quote from an insurer that’s in the 10th percentile ($1,471) or 25th percentile ($1,780), which is cheaper than the median GEICO price. Or, GEICO could even quote you a price that’s lower than their median and you can get an even better deal.

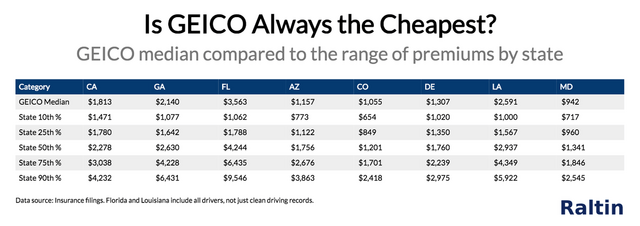

In fact, every state we looked at the median GEICO was cheaper than the state median, but not cheaper than a “10th percentile good deal.”

Source: Raltin

The price variance in the prior chart highlights the importance of comparison shopping since you never know if you’re going to get a great 10th percentile quote or a terrible 90th percentile quote from a carrier. What’s more, in many states even a 25% percentile quote can be cheaper than the median GEICO price.

However, as this analysis shows, GEICO can truthfully make the claim of saving you over 15% on your car insurance. As for whether it takes you just 15 minutes to get the discount, that’s a story for another day.

***

Note: If you’re a company that wants to work with Priceonomics to turn your data into great stories, learn more about the Priceonomics Data Studio.